Identifying the type of property is only one way to break out asset classes. There are also a number of cross-cutting strategies that can be used independent of property type. These strategies cut across all asset classes and shape the deal structure, return profile, and cash flow characteristics of any specific investment. Two investors can own identical properties in the same market and achieve meaningfully different outcomes depending on which strategies they apply.

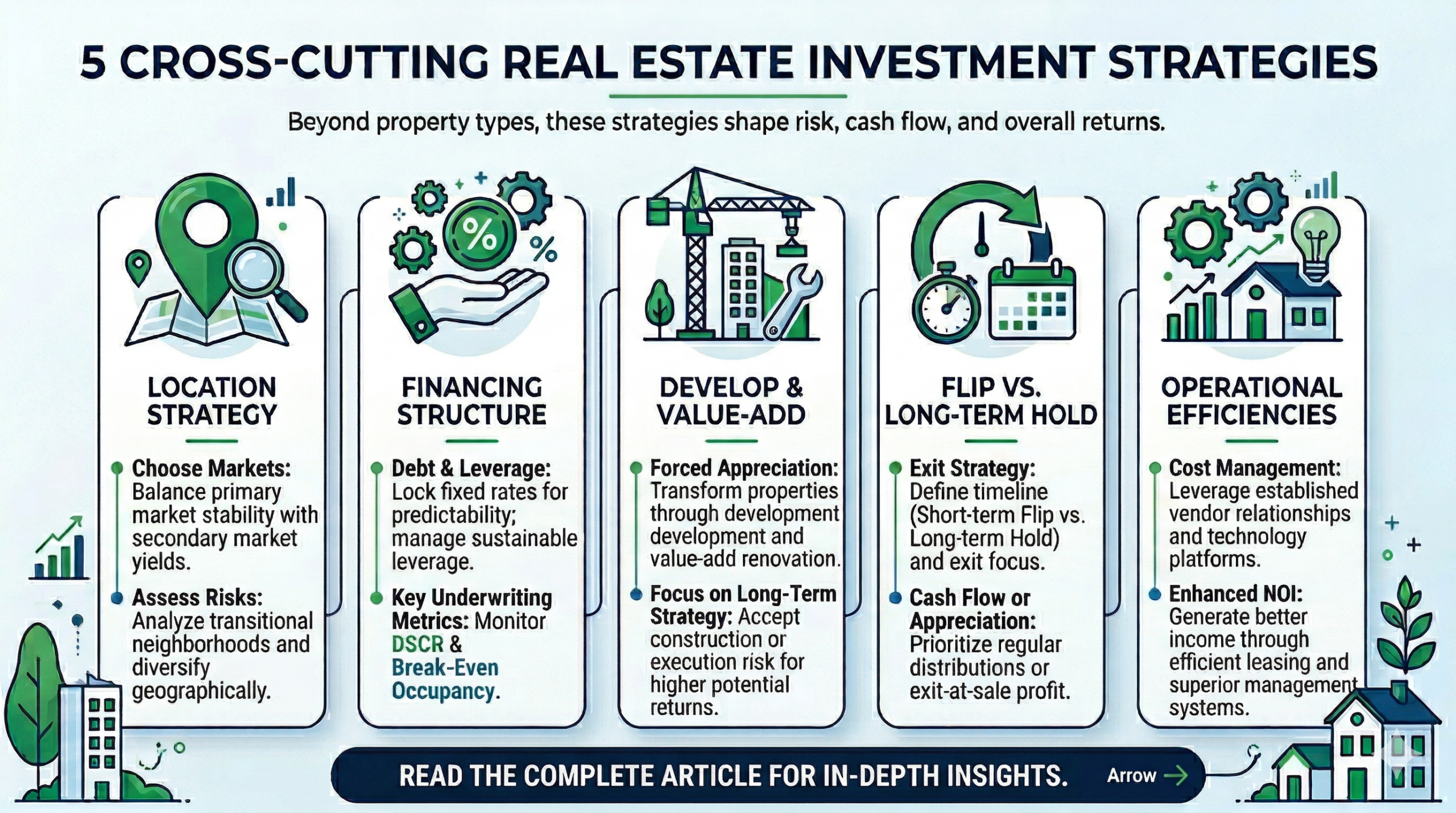

Location

Location is not simply about picking a good neighborhood. It is a deliberate decision about which markets you target and why, and it shapes your risk exposure as much as any other variable.

The most basic dimension is market tier. Primary markets — major urban centers with deep tenant demand and high liquidity — offer stability and ease of exit but typically come with limited returns. Secondary and tertiary markets often offer higher yields, but with less liquidity and greater sensitivity to local economic conditions. Many investors target secondary markets for this reason, accepting the tradeoff in exchange for stronger cash flow.

Your operational plan also impacts which markets you target. Investing in transitional neighborhoods, where demographics, infrastructure, or commercial activity are shifting, can generate outsized appreciation if the transition plays out as anticipated. However, that assumes the transition occurs as planned. Neighborhood improvements can stall, and a property purchased in anticipation of changes that have not yet happened may underperform.

Geographic diversification is another dimension to consider. Concentrating your portfolio in a single market exposes you to local economic disruptions, regulatory changes, and natural disaster risk. Spreading investments across multiple markets reduces that concentration risk. However, it requires a broader operational foundation as you will need to manage teams remotely.

Population migration trends factor heavily into determining appropriate strategies for a location. Markets experiencing sustained inbound migration tend to support rent growth and property appreciation over time. Those losing population face the opposite dynamic, but as a result there may be unique opportunities in those markets. For example, a temporary exodus may reduce prices to the point where there is the opportunity to purchase multiple properties and dominate the market serving the remaining residents. Understanding the underlying drivers of migration such as employment concentration, cost of living, and infrastructure investment helps determine appropriate strategies.

Financing

How a deal is financed is one of the most consequential decisions in any real estate investment, and one that passive investors often underweight in their due diligence. Financing determines how sensitive the investment is to interest rate changes, how much cash flow is available for distributions, and how much risk sits in the capital stack.

The most fundamental distinction is between fixed and floating rate debt. Fixed rate financing locks the interest cost for the loan term, providing predictability in cash flow regardless of what rates do during the hold period. Floating rate debt adjusts with market rates, which can benefit investors when rates fall but can wipe out all of the equity when rates rise. A number of syndication deals that used floating rate bridge loans during the low-rate environment of the early 2020s were unable to manage their operational cash flow when rates rose sharply, eliminating distributions and in some cases resulting in the bank taking over the property.

Leverage level is the second consideration. Higher leverage amplifies returns when a deal performs as projected, but it also amplifies losses when it does not. Conservative leverage ratios preserve more cushion for unexpected expenses, vacancy, or market downturns. As a passive investor, understanding how much debt sits on a property relative to its value, and whether that debt load is sustainable across a range of operating scenarios, is essential underwriting work. The two numbers to look for here are the Debt Service Coverage Ratio (DSCR) and the break even occupancy. The DSCR tells you what percentage of the debt the NOI is projected to cover. Banks usually want a DSCR of at least 1.2% (i.e. the NOI is 120% or more of the debt payment) with higher numbers being better. If the DSCR falls below a certain level, the banks may force certain actions, such as increasing reserves, or be able to call the loan. The break even occupancy tells you how high the vacancy rate can go before the property starts losing money. In this case, the lower the occupancy number, the more cash flow the deal is generating on a monthly basis and the lower the risk.

Loan term and structure also need to be considered. Bridge loans are short-term instruments, typically two to three years, used to finance properties in transition. Permanent financing carries longer terms, and prepayment penalties. As a result, it is more appropriate for stabilized assets generating consistent income that will be held for a long period of time. The structure of the loan should reflect the strategy being pursued and incorporate a margin of safety to account for the operational improvements not going exactly to plan.

Develop and Value-Add

Development and value-add reflect strategies where you are forcing appreciation on a property by improving it in ways that increase your cash flow.

Development creates a new structure from the ground up or involves tearing down most of an existing structure and rebuilding. The majority of the return comes from creating something that did not exist before: a completed building with stabilized occupancy that is worth more than the cost of land and construction. Because no income is generated during the construction period, development deals are appreciation-focused by nature. Cash flow typically begins only after the project reaches stabilization, which may be two to four years after the initial investment. In exchange for that patience and the execution risk carried during construction, development deals often target higher total returns than stabilized acquisitions.

Value-add investing applies a similar logic to existing properties. The asset is acquired below its potential value because it is underperforming: rents are below market, occupancy is low, the physical condition is dated, or some combination of all three. The plan is to close that gap through renovation, improved management, or repositioning, then capture the resulting appreciation through refinancing or sale. During the improvement period, cash flow is typically limited, with no distributions as the capital is used to rebuild the units. Once the business plan is executed and the property stabilizes at its new rent level, distributions begin. Understanding the operator’s specific plan, their track record executing similar plans, and the market’s ability to support the projected rents is the core due diligence work for any value-add investment.

Flip Versus Long-Term Hold

The decision to flip or hold a property is a strategy that can be used independent of property type or other strategies. It determines the investment timeline, the return structure, and the tax implications of the investment.

A flip targets a relatively short hold, anywhere from a few months to five years, during which the operator executes a specific plan and then sells. The return is concentrated at the exit with investors receiving their capital back along with the profit at the sale. Because most of the return comes at disposition rather than through ongoing cash flow, flips tend to be appreciation-focused and are measured primarily by equity multiple and internal rate of return rather than cash-on-cash returns.

Long-term holds prioritize ongoing cash flow and return of capital over exit profit. The operator acquires a stabilized asset, manages it for income over an extended period, and refinances periodically to return capital. The property is expected to be held anywhere from 5 years to indefinitely. This structure suits investors who want regular distributions and are less focused on a near-term liquidity event. While it is usually expected that the property will benefit from long-term appreciation trends, the sale is not the primary focus of these investments. This strategy typically uses cash-on-cash returns and IRR as metrics, and it can lead to the “infinite return” scenario once all of the capital has been returned to the investors.

Operational Efficiencies

Operational efficiency is not the most obvious strategy, but it is often the difference between a deal that meets projections and one that falls short.

Experienced operators bring systematic approaches to cost management: preferred vendor relationships that reduce maintenance and repair costs, technology platforms that reduce management overhead, centralized leasing and administrative functions that spread fixed costs across multiple properties, and energy efficiency improvements that reduce utility expenses. These are not dramatic interventions but cumulative advantages that compound across a multi-year hold.

The implications for passive investors are twofold. First, an operator who has built the systems and relationships to run properties at lower cost will consistently outperform one who has not, even when both are acquiring similar assets at similar prices. Second, operational improvements can themselves be part of the value-add thesis. A well-located property that has been managed poorly may present an opportunity not because of physical renovation, but because a more capable operator can generate significantly better net operating income from the same rent roll.

Summary

Real estate is not a single asset class. It is a multidimensional space defined by property type and strategy. The combinations available are far greater than most investors appreciate when they are first exposed to real estate investing.

The residential asset classes covered in the first article, single family rentals, multifamily properties, and mobile home parks, provide the foundation that most real estate investors build from. They are familiar, financeable, and well understood. The commercial asset classes covered in the second article, raw land, storage, office, and retail, extend that foundation into territory with different legal frameworks, different tenant relationships, and different return profiles. Neither category is inherently superior, each serves different investor goals.

The cross-cutting strategies covered in this article sit on top of both. Location, financing, development and value-add, hold period, and operational efficiency are not asset class decisions. They are strategies that apply regardless of whether you are investing in a multifamily syndication, a strip mall, or a self-storage facility. Two investors in the same asset class pursuing different strategies will have different experiences of risk, cash flow, and return.

For the passive investor, this framework has a practical application. Your investment thesis defines where you want to sit on the dimensions of risk, timeline, cash flow, and return. The property types and strategies covered in these articles are the instruments through which you express that thesis. A conservative investor prioritizing stable cash flow will gravitate toward stabilized assets in primary markets with fixed rate financing and experienced operators focused on efficiency. An investor comfortable with more risk in exchange for higher returns may pursue value-add deals in transitional markets with moderate leverage and a defined exit horizon.

Neither approach is right for everyone. Both can be executed well or poorly. What matters is that your property type and your strategy are consistent with each other and with the goals you established before you started looking at deals.

PS: Are you an adventurer at heart? Always wanted to hang out with thousands of penguins in their natural environment and visit the frozen continent? Join me and a small group of real estate investors for an exclusive workshop aboard an expedition cruise to Antarctica in February 2027. Build lifelong relationships while exploring one of Earth’s last pristine wildernesses. To learn more and reserve your cabin go to https://www.mbc-rei.com/2027 Have questions? Email me at events@mbc-rei.com.

The complete set of newsletter archives are available at:

https://www.mbc-rei.com/mbc-thoughts-on-passive-investing/

This article is my opinion only, it is not legal, tax, or financial advice. Always do your own research and due diligence. Always consult your lawyer for legal advice, CPA for tax advice, and financial advisor for financial advice.