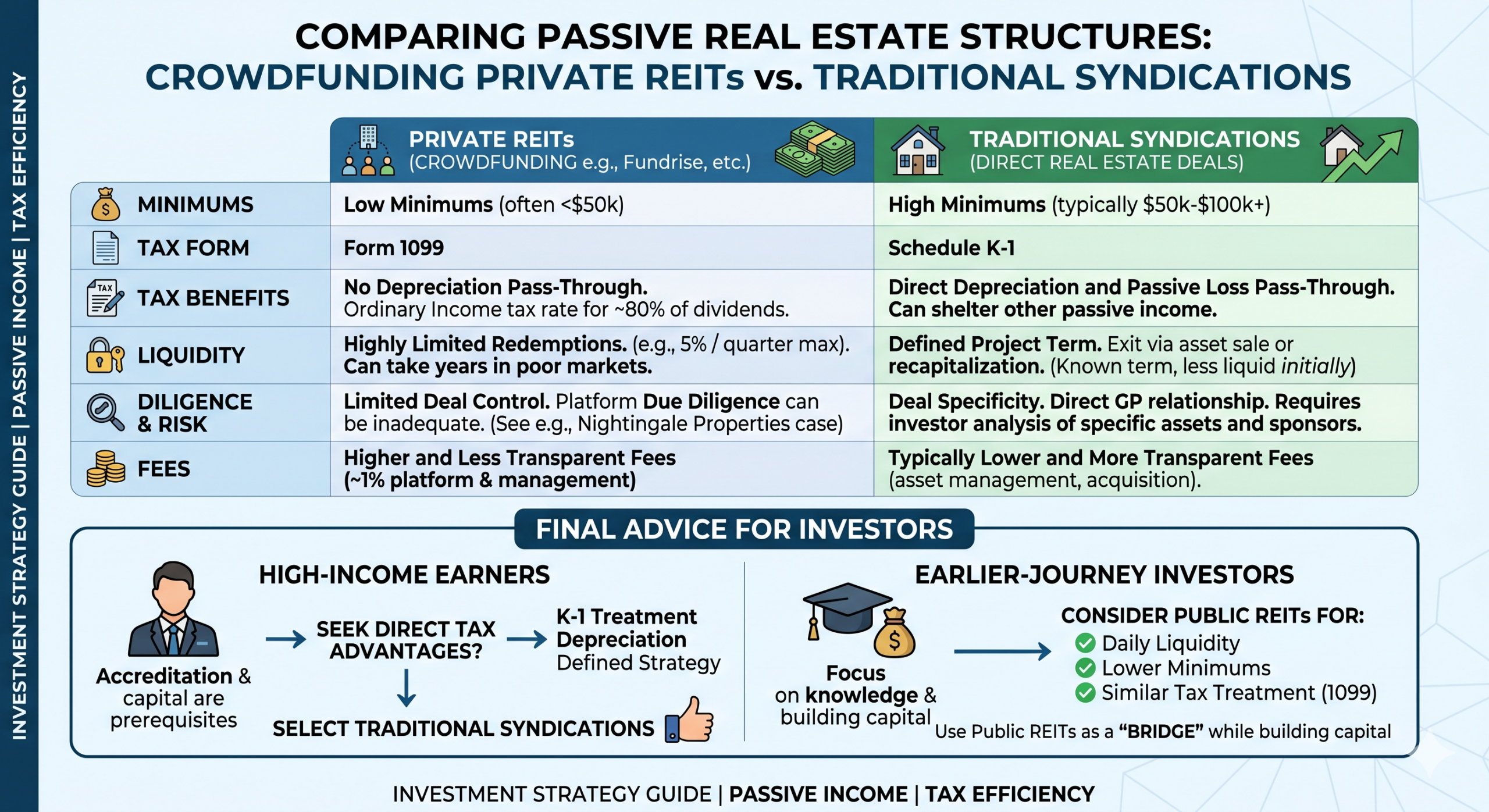

As someone who focuses on passive income investing, I receive regular questions about real estate crowdfunding platforms such as Fundrise and CrowdStreet. The appeal is easy to understand. These platforms market deals with low minimums, often well below the $50,000 to $100,000 typically required to participate in a syndication. They claim to vet sponsors before listing deals on their platforms, reducing the due diligence burden on the investor. And they offer a wide selection of opportunities, including private equity vehicles, that appear to provide meaningful diversification.

For certain investors, these platforms can be useful. If you are not yet accredited, if you are earlier in your investing journey, or if you simply want some exposure to real estate without committing significant capital, a crowdfunding platform can be a reasonable starting point. There is nothing wrong with using these tools as a bridge while you build the knowledge and capital to access traditional syndications.

However, if you are a high-income earner looking to build meaningful passive cash flow and break your paycheck dependency, I suggest carefully examining these platforms before you deploy significant capital. What they offer is often quite different from what the marketing implies.

How These Platforms Have Evolved

Real estate crowdfunding platforms originally positioned themselves as marketplaces: connecting general partners who needed capital with limited partners who had it. The JOBS Act made this model broadly accessible beginning in 2012, and platforms like CrowdStreet and Fundrise grew rapidly on the promise of democratizing access to commercial real estate.

Over time, both platforms moved away from pure matchmaking and toward running their own pooled fund structures. This evolution matters because the investment you are making today bears little resemblance to a traditional real estate syndication. In many respects, you are purchasing something closer to a non-traded REIT than a direct stake in a specific property.

Platform Risk

Before examining the structural characteristics of these funds, it is worth addressing a risk that the marketing materials rarely mention: the platform itself can be a source of loss.

CrowdStreet’s Nightingale Properties case illustrates this directly. In 2022, Nightingale raised more than $63 million from over 800 investors across two offerings on the CrowdStreet platform, including what was at the time the largest single fundraise in CrowdStreet’s history. Neither deal closed. Nightingale CEO Elie Schwartz pleaded guilty to fraud, and a federal court sentenced him to 87 months in prison in 2025. [1] Investors alleged that CrowdStreet had released funds before deals closed and failed to conduct adequate due diligence on the sponsor. [2]

The point is not to single out CrowdStreet. Fraud can occur in any investment, including traditional syndications. The point is that “the platform vets the deals” is not a substitute for your own due diligence. When a platform fails to catch a fraudulent sponsor, and you do not conduct independent analysis, you have no secondary line of defense. The CrowdStreet investors who lost money were relying entirely on a third party to protect them. That is a precarious position regardless of the investment vehicle.

Examining the Fundrise Flagship Real Estate Fund

To understand what these platforms are actually offering today, let’s examine one of their products in detail. The Fundrise Flagship Real Estate Fund is a useful case study, though this analysis represents my opinion only and should not be considered investment, tax, or legal advice.

The fund’s current annualized return and its monthly distribution rate have varied since inception. Before investing in any fund, you should review the most recent figures directly from the fund documents rather than relying on marketing materials, as these numbers change over time. At the current time, they are presenting a 4.3% annualized return on investment with a highly variable monthly distribution rate. That is less than what you can get with a 10 year treasury.

What matters even more are the structural characteristics that shape the investment returns across the holding period. The fund is structured and taxed as a REIT. In a traditional syndication, your investment generates a K-1 tax form each year. This allows you to take depreciation and other passive losses directly on your tax return, which can shelter a meaningful portion of your income. The Fundrise fund issues a 1099 instead of a K-1, because the REIT election shifts the tax treatment. Distributions are taxed as REIT dividends rather than pass-through income, which means you do not receive the depreciation benefit. Approximately 80% of the dividend income received is taxable at your ordinary income rate, with some portion potentially treated as return of capital.

Liquidity is also an important consideration. Crowdfunding platforms frequently promote the idea that you can access your capital easily. The fund documents tell a more qualified story. Redemptions are typically limited to 5% of outstanding shares per quarter under normal circumstances. If redemption requests spike, that percentage can be reduced further across all sellers simultaneously. In a scenario where many investors seek to exit at the same time, which tends to happen during exactly the market conditions when you most want access to your capital, it could take several years to fully liquidate your position. Thus, in the worst case, your liquidity is similar to a typical syndication deal and very different from a publicly traded REIT.

The fund charges a 0.85% management fee plus a 0.15% platform fee, totaling 1.0% annually. That fee level is in line with what many syndication sponsors charge. The difference is that in a syndication, you are receiving K-1 treatment, direct depreciation benefits, and a stake in a specific asset with a defined business plan. In a REIT structure, you are paying a comparable fee for a vehicle that has more in common with a publicly traded REIT than a real estate partnership.

When Does Structure Make Sense?

This brings up a key question worth considering: why invest in a private REIT? If you want REIT-style exposure to real estate, publicly traded REITs are available at minimal transaction cost, with daily liquidity, through any brokerage account. Several large, publicly traded REITs have long operating histories and meaningful dividend yields. If your primary goal is ease of access and you accept REIT tax treatment, that option is straightforward and does not require locking up capital for an extended period.

If, on the other hand, you are willing to accept illiquidity in exchange for tax benefits and direct participation in specific assets, a traditional syndication with an experienced sponsor offers a structurally different proposition: K-1 treatment, depreciation pass-through, and a defined investment thesis with a clear exit strategy.

The crowdfunding fund structure, as currently offered by platforms like Fundrise, sits in between these two options. It carries the illiquidity of a private investment without the full tax advantages. It offers the simplicity of a pooled fund without the liquidity of a publicly traded security.

From my perspective, the private REITs take the worst from both sides and combines them, making them an inferior option. For high-income earners who have the accreditation status and the willingness to do the due diligence required to access traditional syndications, those can be a better option as you reap the benefits of the illiquidity premium those provide. For those who are earlier in their investing journey or building toward that threshold, public REITs seem to provide a better option than crowdfunding platforms as they have similar tax treatments and better liquidity.

As always, understanding what you are actually purchasing and how it fits in to your overall investment thesis is the prerequisite for making an informed choice.

Sources

[1] Propmodo, “Nightingale Properties CEO Gets Hefty Sentence for CrowdStreet Fraud,” May 2025. https://propmodo.com/nightingale-properties-ceo-gets-hefty-sentence-for-his-involvement-in-the-crowdstreet-fraud/

[2] Bisnow, “Investors Seek To Shut Down CrowdStreet After Nightingale Fiasco,” February 2024. https://www.bisnow.com/national/news/office/customers-seek-to-shut-down-crowdstreet-after-nightingale-fiasco-122707

The complete set of newsletter archives are available at:

https://www.mbc-rei.com/mbc-thoughts-on-passive-investing/

This article is my opinion only, it is not legal, tax, or financial advice. Always do your own research and due diligence. Always consult your lawyer for legal advice, CPA for tax advice, and financial advisor for financial advice.

PS: I am building a community of successful investors that love adventure travel. If that sounds like you, email me to join our free Discord community where we can share tips, tricks, and maybe travel together.