Most investors understand that diversification matters and that having a single asset in their investment portfolio is extremely risky. Fewer understand what it actually means to be well diversified. Holding a collection of technology stocks is not diversification. Owning several apartment buildings in the same city is not diversification. True diversification operates across four distinct dimensions, and understanding each one is required to build a portfolio designed to generate reliable passive income for decades.

The core advantage of diversification is straightforward: by spreading capital across multiple assets, you smooth out portfolio performance by averaging results rather than depending on a single outcome. You will not capture the extraordinary gains of an investor who put everything into NVIDIA two years ago. You will also avoid the catastrophic losses of someone whose entire net worth sat in Enron or Kodak when those companies collapsed. Diversification is an acceptance that average, consistent returns across a portfolio are worth more than the lottery ticket of concentrated bets, particularly when your goal is cash flow that replaces a paycheck, not a one-time windfall.

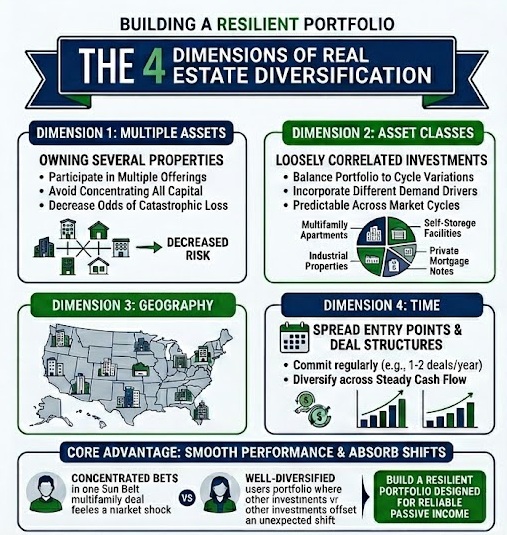

Dimension #1: Multiple Assets

The foundation of any diversification strategy is holding multiple distinct assets rather than a single one. For stock investors, this means owning shares across different companies. For real estate investors, it means holding multiple properties. For passive investors deploying capital into syndication deals, it means participating in multiple offerings rather than concentrating everything into one.

The reasoning is simple. A single asset carries the full weight of its own risk. In stocks, one company’s failure wipes out the position entirely. In direct real estate, a single vacancy or fire damage event can eliminate cash flow entirely while expenses continue. In syndications, a single deal gone wrong, whether due to market conditions, operator error, or circumstances no one anticipated, can result in a partial or total loss of invested capital.

Holding multiple assets does not eliminate this risk. It decreases the odds that when one investment underperforms, the results on your portfolio are catastrophic. The impact of any individual failure is absorbed across the portfolio.

Dimension #2: Asset Classes

Within any single asset class, investments tend to move together. Technology stocks correlate with each other. Small apartment buildings respond to similar macroeconomic pressures. When interest rates rise sharply, many asset classes feel the impact simultaneously—though not equally, and not on the same timeline.

By selecting asset classes that are loosely correlated with each other, you incorporate assets that will behave differently depending on where each sits in its own cycle. Within a brokerage account, this might mean balancing an S&P 500 index fund with growth stocks, commodities or bonds. Within real estate, it might mean holding positions across apartment buildings, self-storage facilities, industrial properties, and private mortgage notes.

Multifamily syndications have been the dominant deal type for much of the past decade, and many passive investors find themselves with significant concentration in a single asset class without realizing it. Adding exposure to industrial, medical office, or note-based investments, each with their own demand drivers and economic sensitivities, creates a portfolio that behaves more predictably across full market cycles.

Dimension #3: Geography

Different cities, states, and countries operate under different economic conditions, regulatory environments, and demographic trends. A landlord-friendly state can become less so after a single legislative session. A city experiencing strong population growth can stagnate when a dominant employer relocates. Markets that appear stable over a three-year horizon can shift materially over ten.

Geographic diversification reduces exposure to any single regulatory or economic environment. In a brokerage portfolio, this typically means incorporating international holdings alongside domestic ones. In real estate, it means investing across different cities or states rather than concentrating in a single market.

Passive syndication investing makes geographic diversification more accessible than direct ownership. An investor can hold positions in deals located across multiple states without the operational complexity of managing properties in multiple jurisdictions. This is one of the structural advantages of the syndication model.

Dimension #4 Time

No investor consistently times markets well. Attempting to do so introduces a risk that diversification across the other three dimensions does not address: the risk of concentrating your purchases at the wrong point in a cycle.

In public markets, dollar cost averaging addresses this by investing fixed amounts at regular intervals, capturing both high and low prices over time and averaging the entry point across a full market cycle. A comparable discipline applies to real estate. An investor who commits to one or two syndication deals per year, regardless of market sentiment, builds a portfolio with entry points spread across multiple stages of the cycle rather than concentrated at a single peak.

Time diversification also applies to deal structure. Investing across deals at different stages (i.e. new construction projects, value-add repositioning plays, and stabilized cash-flowing assets) creates a portfolio where some positions are generating current income while others are building toward a larger appreciation event at exit. Each structure has a different timeline and a different return profile. Holding all three simultaneously means the portfolio is rarely sitting entirely idle while waiting for a single outcome.

Summary

Diversification smoothes investment returns and reduces the probability of a single event causing catastrophic losses. For the passive investor whose goal is generating reliable cash flow to replace employment income, this matters more than it might for someone chasing maximum returns on a short timeline.

The investor who holds positions across multiple syndication deals, spanning several asset classes, located in different geographic markets, entered at different points in the cycle, has built something structurally different from the investor who has placed capital into three multifamily deals in the same Sun Belt city. Both may perform well in favorable conditions. Only one is built to absorb an unexpected shift.

The goal is not to optimize any individual position. It is to build a portfolio resilient enough to keep generating cash flow through the conditions you cannot predict.

The complete set of newsletter archives are available at:

https://www.mbc-rei.com/mbc-thoughts-on-passive-investing/

This article is my opinion only, it is not legal, tax, or financial advice. Always do your own research and due diligence. Always consult your lawyer for legal advice, CPA for tax advice, and financial advisor for financial advice.