Most investors who transition from residential to commercial real estate do so because they are looking for scale. A single multifamily syndication can deploy more capital, generate more cash flow, and require less per-dollar management effort than a portfolio of single family rentals assembled over years. Commercial real estate makes that scale accessible, but it does so across a surprisingly varied landscape.

The previous article covered residential asset classes: single family rentals in their three forms, multifamily properties, and mobile home parks. Each of those categories shares the common thread of providing housing to people who live in your property. Commercial real estate operates on different assumptions. Your tenants are businesses or individuals engaging in activities outside of their homes. The legal frameworks differ. The lease structures differ. The financing differs. And the risk and return characteristics differ.

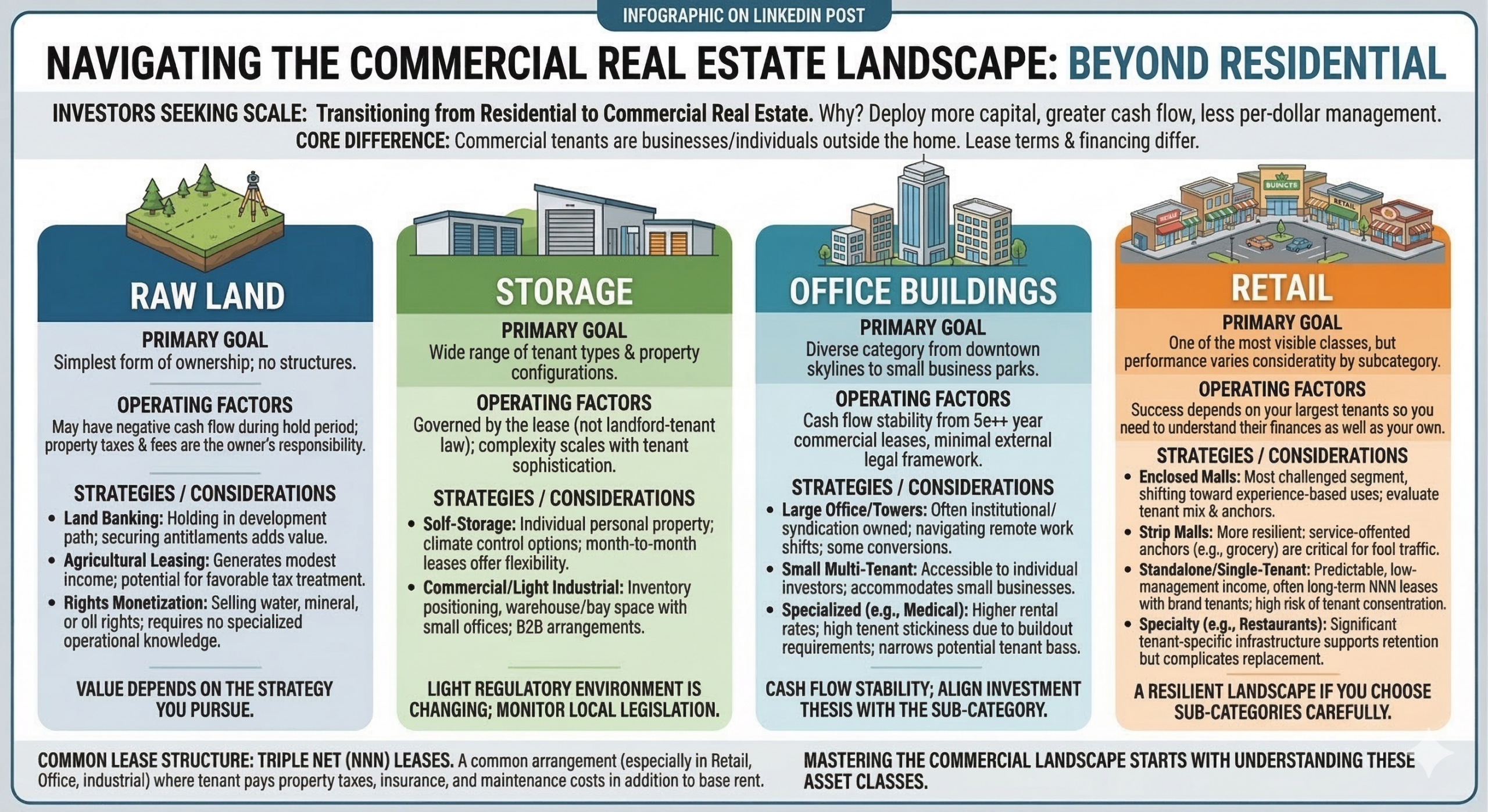

One lease structure that appears across most commercial categories is the triple net, or NNN, lease. Under this arrangement, the tenant pays not only base rent but also property taxes, insurance, and maintenance costs. This shifts a significant portion of operating expense and variability onto the tenant, which simplifies the ownership experience and makes cash flow more predictable for the investor. NNN leases are particularly common in retail and office, and appear frequently in industrial properties as well. When you encounter a commercial opportunity, confirming whether the lease is gross, modified gross, or NNN is one of the first questions worth asking, as it directly affects how you should evaluate the net income the property generates.

This article examines four commercial categories: raw land, storage, office, and retail with the understanding that the commercial landscape extends further than any single chapter can fully address. The goal, as with residential asset classes, is not to master all of it. It is to understand enough of the landscape to identify which corners of it align with your investment thesis, then develop genuine expertise there.

Raw Land

Raw land is the simplest form of real estate ownership. There are no structures to maintain, no tenants to manage, and no property management overhead. What you own is the underlying asset itself, and how you extract value from it depends entirely on which of three strategies you pursue: land banking, agricultural leasing, or rights monetization.

Land banking is the most straightforward. You acquire land, hold it, and wait for appreciation. The strategy works best when you can identify property in the path of development and purchase it before that trajectory is reflected in the price. When the land becomes a viable development candidate, you can sell it outright or develop it directly. Securing entitlements in advance, including zoning changes, subdivision approvals, and easements, removes uncertainty for potential buyers and compresses their development timeline. That reduction in risk translates directly into a higher price for the seller. The major downside is that there is no positive cash flow coming in while you hold the property, yet you are responsible for expenses such as property taxes and permit fees.

Agricultural leasing generates income during the hold period. The owner leases the land to a local farmer or rancher who handles all operations. Lease terms vary considerably, from one year to twenty years or more, depending on the use. Rents are typically modest compared to residential properties, but carrying costs are equally low. In many jurisdictions, agricultural use also qualifies the property for favorable property tax treatment, which reduces the net cost of holding the land while you wait for appreciation.

Rights monetization takes a different approach. Many parcels carry associated rights, including water, mineral, oil, or air rights that have independent value. These can be leased to parties with the expertise and equipment to extract the underlying resource. A water rights lease, for example, might give the lessee access to drill and sell from an aquifer on your property. The owner contributes the right; the lessee contributes the operational expertise. The income flows without requiring the owner to develop any specialized knowledge.

Storage

Storage is a commercial asset class that spans a wide range of tenant types and property configurations. The legal environment differs fundamentally from residential real estate: because you are not providing housing, landlord-tenant law does not apply. The governing document is the lease itself, and the complexity of that lease scales with the sophistication of the tenant.

Self-storage serves individuals storing personal property. The range of product is wide, from open-air parking for boats and RVs to climate-controlled units for wine collections or archival records. Operations and maintenance complexity vary accordingly. Leases are typically month-to-month, allowing both the tenant and the owner significant flexibility. One notable development in this segment is pressure for new regulations in several jurisdictions in response to consumer complaints about significant rent increases. Investors entering self-storage should monitor local legislative activity, as the historically light regulatory environment may change in specific markets.

Commercial tenants use self-storage as well, primarily for inventory positioning, but their needs frequently extend into light industrial storage and warehouse space. Light industrial storage accommodates large quantities of inventory in a single location, often in outdoor or minimally covered configurations. When protection from the elements is required, tenants move into warehouse and bay industrial space, which typically includes a small office component alongside the storage area. Because the counterparty in these arrangements is another business, the lease agreement carries the full weight of the relationship and there are minimal external legal requirements.

Office Buildings

The office category covers more ground than the downtown skyline suggests. Large multi-tenant towers, small multi-tenant buildings, and specialized medical or professional facilities each occupy distinct positions in this asset class.

Large office buildings, the towers that anchor urban cores, often contain hundreds of thousands of rentable square feet distributed across dozens of tenants. The ideal configuration places one tenant per floor, though smaller tenants routinely share floors in buildings with 20,000 to 40,000 square feet per level. Properties of this scale are typically owned through syndications or institutional funds. This asset class has navigated a difficult period as remote work reduced demand, but vacancy rates have been declining as some buildings convert to alternative uses and more employers require in-office attendance on a regular basis.

Smaller multi-tenant office buildings, those sized to accommodate one to ten small businesses, present a more accessible entry point for individual investors. These properties carry the same favorable lease characteristics as their larger counterparts: commercial leases run five years or longer as a standard, providing cash flow stability that residential properties rarely match. Because both parties to the lease are businesses, the legal framework is minimal and the lease itself must be explicit about each party’s obligations.

Specialized office properties introduce a further variable. Medical and dental facilities require building infrastructure that standard office space does not provide: additional plumbing, higher electrical capacity, patient rooms, and specific layout configurations. These requirements narrow the potential tenant base. They also support higher rental rates from the tenants who do fit the profile, and they create a degree of tenant stickiness, since a medical practice that builds out a space to its specifications is unlikely to relocate without a compelling reason.

Retail

Retail real estate is one of the most visible commercial asset classes with storefronts, shopping centers, and restaurants occupy nearly every commercial corridor in every market. While the struggles of large enclosed malls have been well publicized, performance across retail subcategories varies considerably, and understanding those distinctions is important.

Enclosed malls represent the most challenged segment of retail. The rise of e-commerce compressed foot traffic at many properties over the past decade, and a number of large enclosed malls have experienced significant vacancy as anchor tenants closed or consolidated locations. In some cases, the buildings have been shuttered completely. The properties that have performed best through this period are those that shifted their tenant mix toward experience-based uses — dining, entertainment, and fitness — that cannot be replicated online. In other cases, the buildings have simply been converted into other uses such as storage or office space. Investors considering enclosed malls should evaluate the property’s tenant mix, anchor situation, and surrounding market demographics as performance within this subcategory varies widely.

Strip malls have been more resilient. These open-air configurations, anchored by service-oriented tenants such as grocery stores, pharmacies, and quick-service restaurants, have maintained stronger occupancy. While these are typically neighborhood gathering points, servicing a local area, a unique mix of stores can elevate the property to a regional destination. The anchor tenant is critical as a well-performing store generates consistent foot traffic that benefits every other tenant. As a result, when evaluating a strip mall investment, the anchor’s lease term and financial health deserve as much attention as the overall occupancy rate and property location.

Standalone retail buildings are single-tenant properties leased to one occupant, often a national or regional brand. Fast food restaurants, pharmacies, and banks are common examples. These properties frequently carry NNN leases with long initial terms, sometimes fifteen to twenty years, and scheduled rent increases built into the lease structure. The result is a predictable, low-management income stream for the duration of the lease. The primary risk is tenant concentration: the entire property’s income depends on a single occupant, so the financial strength and lease term of that tenant are the most consequential underwriting variables.

Specialty retail includes formats with specific operational or physical requirements. Restaurants are the most common example. A restaurant buildout involves significant tenant-specific infrastructure, such as commercial kitchens, ventilation systems, grease traps, hood suppression systems, that a subsequent tenant may or may not be able to use. This creates two dynamics worth understanding. First, a restaurant tenant who has invested heavily in a buildout has a practical incentive to remain in the space, which supports lease renewal. Second, if that tenant does vacate, re-leasing the space to a non-restaurant user typically requires substantial renovation, which affects the owner’s re-tenanting cost and timeline. Other specialty formats, including entertainment venues, and fitness facilities, carry similar considerations: specialized infrastructure that supports retention but complicates replacement.

Summary

Residential and commercial real estate together cover the spectrum of asset classes available to a passive investor. Residential properties, covered previously, provide housing and operate under landlord-tenant frameworks that shape every aspect of the ownership experience. Commercial properties serve businesses, operators, and individuals in non-housing contexts, and they are governed primarily by the lease agreements that both parties negotiate and sign.

Within commercial real estate, the categories examined here, raw land, storage, office, and retail, illustrate how differently the investor experience can look depending on which asset class you choose. Land requires patience and carries no management burden. Storage operates at the simpler end of commercial leasing, with the primary challenge being addressing high turnover resulting from monthly leases. Office properties offer long lease terms and cash flow stability, with specialized subcategories that trade a narrower tenant base for higher rents and stronger tenant retention.

What unifies all of these asset classes, residential and commercial alike, is that the category itself is only part of the investment decision. What you do with the property once you purchase it is as consequential as which asset class you select. Those decisions reflect the cross-cutting strategies that are the subject of the next article.

PS: Are you an adventurer at heart? Always wanted to hang out with thousands of penguins in their natural environment and visit the frozen continent? Join me and a small group of real estate investors for an exclusive workshop aboard an expedition cruise to Antarctica in February 2027. Build lifelong relationships while exploring one of Earth’s last pristine wildernesses. To learn more and reserve your cabin go to https://www.mbc-rei.com/2027 Have questions? Email me at events@mbc-rei.com.

The complete set of newsletter archives are available at:

https://www.mbc-rei.com/mbc-thoughts-on-passive-investing/

This article is my opinion only, it is not legal, tax, or financial advice. Always do your own research and due diligence. Always consult your lawyer for legal advice, CPA for tax advice, and financial advisor for financial advice.