Outside of depreciation, the 1031 exchange is one of the most favorable tax treatments available to real estate investors. Named for Section 1031 of the Internal Revenue Code, a 1031 exchange allows an investor to sell a property and, if certain rules are followed, to roll any gains from that property into a newly purchased property while deferring the taxes that would otherwise be due.

For context, consider how the tax code treats stock investments. When you sell shares of stock at a profit, you owe capital gains taxes on those gains in the year of the sale. The IRS collects its share immediately, reducing the capital you have available to reinvest. Real estate investors using a 1031 exchange face no such immediate tax consequence. By deferring these taxes, you retain more capital to deploy into your next investment, which allows you to purchase a larger property or set of properties and accelerates your wealth-building trajectory.

This tax advantage becomes particularly powerful when executed repeatedly over time. Each exchange preserves your full capital base for reinvestment, allowing your wealth to compound at a faster rate than would be possible in taxable transactions. Understanding the mechanics and requirements of 1031 exchanges is essential for any investor building a direct real estate portfolio. As always, remember that I am not a tax professional. Consult with your own professional team before making any decisions.

Understanding the Critical 1031 Rules

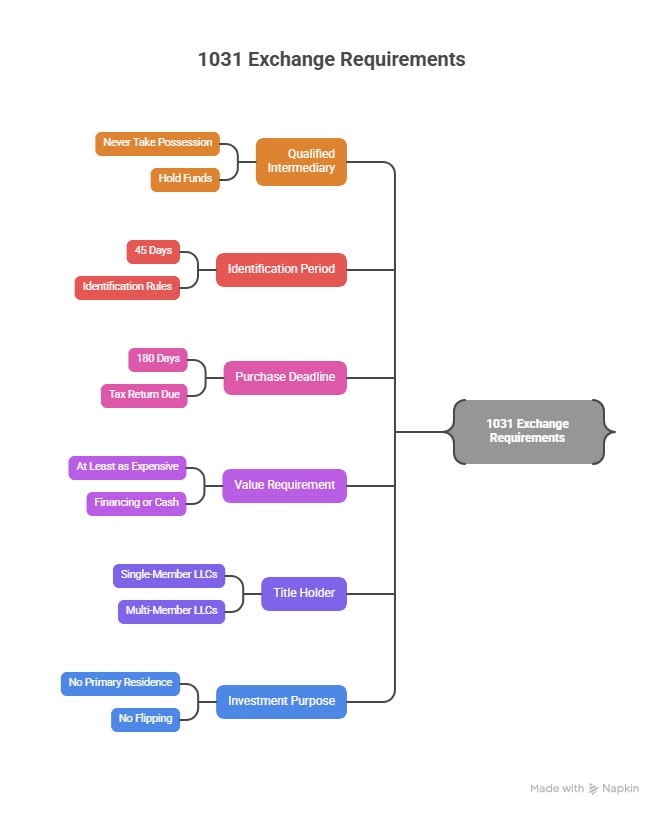

The rules governing 1031 exchanges are unforgiving. If you fail to follow them exactly, you will not qualify for the tax benefits and will owe taxes on your gains in the year of sale. There are six requirements:

- Use a qualified intermediary and never take direct possession of sale proceeds. You cannot receive the money from your property sale, even temporarily. A qualified intermediary must hold the funds from the moment of sale until they are used to purchase the replacement property. Taking possession of the proceeds disqualifies the entire exchange.

- Identify the replacement property within 45 days of closing on the sale. You must identify specific properties in writing and send the documentation to your intermediary before the 45-day window closes. There are three identification rules: you can identify any three properties regardless of value; you can identify any number of properties as long as their total value does not exceed 200 percent of the sales price of the original property; or you can identify any number of properties as long as you ultimately purchase properties totaling at least 95 percent of the total value identified. The first option is by far the most commonly used.

- Complete the purchase within 180 days of the original sale or before your tax return is due, whichever comes first. The replacement property purchase must close within this timeframe. If you sell your property late in the year, your tax filing deadline may arrive before the 180-day window closes, which effectively shortens your timeline.

- Purchase a replacement property at least as expensive as the property you sold. If your replacement property costs less than your sale price, you will owe taxes on the difference. This requirement is based on the sales price of the properties, not on the equity you held. To fully defer all taxes, you must either obtain financing on the new property at least equal to the loan amount on the property you sold, or you must contribute additional cash to make up any difference.

- Hold title to both properties in the name of the same taxpayer(s). Single-member LLCs that are disregarded entities for tax purposes can have different legal names as long as they are owned by the same individual. However, for multi-member LLCs, ownership must remain identical between the old and new properties.

- Hold both properties for investment purposes. You cannot exchange into or out of your primary residence. Neither property can be intended as a flip for quick resale. Properties acquired for resale are generally considered inventory rather than investment assets and are taxed under different rules.

These rules can create significant pressure for investors attempting to complete an exchange. The 45-day identification window and 180-day closing deadline are particularly challenging. Sellers of properties you have identified can leverage these deadlines against you, extracting better terms or threatening delays once you have passed the 45-day mark and have no flexibility to identify alternative properties. To minimize this risk, best practice is to have a purchase contract in place as early as possible, ideally before you even sell your original property, so the seller cannot use your deadline pressure as negotiating leverage

How Your New Property Basis is Calculated

While a 1031 exchange allows you to defer capital gains taxes on the sale of your original property, those gains are deferred, not eliminated. The tax liability follows you to the new property through the mechanism of basis calculation. The basis in your new property equals the purchase price of that property minus any deferred gain. The deferred gain equals the sales price of your original property minus its adjusted basis at the time of sale.

Consider this example: You sell a property for $500,000, and your adjusted basis in that property is $200,000. Thus your gain is $300,000. If you purchase a replacement property for exactly $500,000, your basis in the new property will be $200,000. The $300,000 gain has been deferred, not eliminated, which is reflected in your reduced basis.

If you instead purchase a replacement property for $750,000, your basis would be $450,000. You started with a $750,000 purchase price and subtracted the $300,000 deferred gain.

It is the adjusted basis, not the purchase price, that you use to calculate depreciation deductions on the new property. Exchanging into a similarly priced property limits your future depreciation deductions because your basis remains low. To maximize ongoing tax benefits, investors typically purchase properties substantially more expensive than the properties they sold, which increases their basis and provides larger depreciation deductions going forward.

Planning Your Exit

At some point, you will sell an investment property for the last time. This final disposition occurs either because you pass away while owning the property and your heirs sell it, or you decide to exit real estate investing.

The inheritance scenario provides additional tax benefits. When you pass away while owning property, your heirs receive a step-up in basis to the fair market value of the property on the date of your death. This step-up in basis eliminates all accumulated deferred gains, even those resulting from exchanges.

Consider an example: You purchased a property decades ago for $200,000. Through multiple 1031 exchanges, you have deferred gains totaling $800,000. The property you currently hold is worth $1,500,000 at your death. Your heirs inherit the property with a basis of $1,500,000. If they sell immediately for $1,500,000, they owe no capital gains taxes whatsoever. The $800,000 in deferred gains and the $500,000 in appreciation since your last exchange all escape taxation entirely.

This favorable treatment has led to the phrase “1031 till you die” becoming a cornerstone tax planning strategy for many real estate investors. By continuing to exchange properties throughout your lifetime and never triggering a taxable sale, you can pass substantial wealth to your heirs completely free of capital gains taxes.

If you choose to sell a property during your lifetime without participating in another exchange, you will owe taxes on all deferred gains. While this tax bill may be substantial, particularly if you have participated in several exchanges over many years, the deferral strategy has still provided significant value. The time value of money means that dollars paid in taxes 10, 20, or 30 years from now are worth considerably less than the dollars you would have paid earlier, even without accounting for inflation. You have had the use of that capital throughout the intervening years to generate additional returns.

The Lazy Exchange

Selling a property and choosing not to perform a 1031 exchange does not necessarily mean abandoning real estate investing. Several situations might lead you to this decision. You may be invested as part of a group where other members want to receive their capital back in cash. You may have been unable to identify a suitable replacement property within the 45-day window. You may be investing in syndications, where the ownership structure makes traditional 1031 exchanges impossible.

An alternative approach has gained popularity in recent years, particularly among passive investors. This strategy, sometimes called a “lazy 1031,” involves selling a property, claiming the gains on your taxes, and then using the depreciation deductions from a newly purchased property to offset those gains on the same tax return.

This approach has become increasingly valuable as cost segregation studies and bonus depreciation have dramatically accelerated the deduction available in the first year of property ownership. It is often possible to generate first-year depreciation losses large enough to completely offset the capital gains from a property sale that occurred in the same tax year.

As an example: You sell a rental property and realize a $300,000 capital gain. Ordinarily, you would owe capital gains taxes on this amount. However, instead of spending that money or putting it in the stock market, you put all of it into a real estate syndication in the same tax year. That syndication performs a cost segregation study and utilizes bonus depreciation, generating $350,000 in depreciation losses allocated to you as a limited partner. On your tax return, the $350,000 depreciation loss offsets the $300,000 capital gain, resulting in a net $50,000 loss. You owe no taxes on the property sale, and you carry forward the remaining $50,000 loss to offset future income.

This strategy offers several advantages compared to traditional 1031 exchanges. It eliminates the strict 45-day identification deadline and the 180-day closing requirement. It does not require matching loan amounts or purchase prices between properties.

The primary timing requirement is that both the sale and the purchase must occur within the same tax year so the gains and losses appear on the same tax return. If the purchase occurs in the following year, you will have already filed your tax return and paid taxes on the gain from the sale, so the losses will just carry forward instead of being used to offset the gain.

This approach is particularly valuable for investors who participate in real estate syndications as passive limited partners. Traditional 1031 exchanges are not available in these situations due to the ownership structure. This strategy of offsetting gains with accelerated depreciation provides similar tax deferral benefits without requiring direct property ownership or the complexity of exchange requirements.

Summary

A 1031 exchange is a powerful mechanism for indefinitely deferring taxes on gains from investment real estate. For investors building direct property portfolios, the ability to preserve capital and reinvest it without tax consequences accelerates wealth accumulation substantially compared to taxable transactions. The step-up in basis at death can eliminate deferred gains entirely for your heirs, making “1031 till you die” an effective long-term tax strategy.

However, the strict rules governing these exchanges create implementation challenges. The compressed timelines and the potential for sellers to exploit your deadline pressure all add complexity to what might otherwise be straightforward real estate transactions.

The alternative approach of using accelerated depreciation to offset gains provides similar benefits for investors who cannot or choose not to pursue traditional 1031 exchanges. This strategy works particularly well for passive investors in syndications and eliminates many of the most burdensome requirements of formal exchanges.

Understanding both strategies allows you to select the approach that best fits your specific situation. Direct property owners building portfolios over time will generally benefit from traditional 1031 exchanges. Passive investors in syndications and those seeking greater flexibility may find the depreciation offset strategy more practical. Both approaches serve the same ultimate goal: minimizing taxes to maximize the capital available for building wealth and generating the passive income that breaks your paycheck dependency.

PS: Are you an adventurer at heart? Always wanted to hang out with thousands of penguins in their natural environment and visit the frozen continent? Join me and a small group of real estate investors for an exclusive workshop aboard an expedition cruise to Antarctica in February 2027. Build lifelong relationships while exploring one of Earth’s last pristine wildernesses. To learn more and reserve your cabin go to https://www.mbc-rei.com/2027 Have questions? Email me at events@mbc-rei.com.

The complete set of newsletter archives are available at:

https://www.mbc-rei.com/mbc-thoughts-on-passive-investing/

This article is my opinion only, it is not legal, tax, or financial advice. Always do your own research and due diligence. Always consult your lawyer for legal advice, CPA for tax advice, and financial advisor for financial advice.